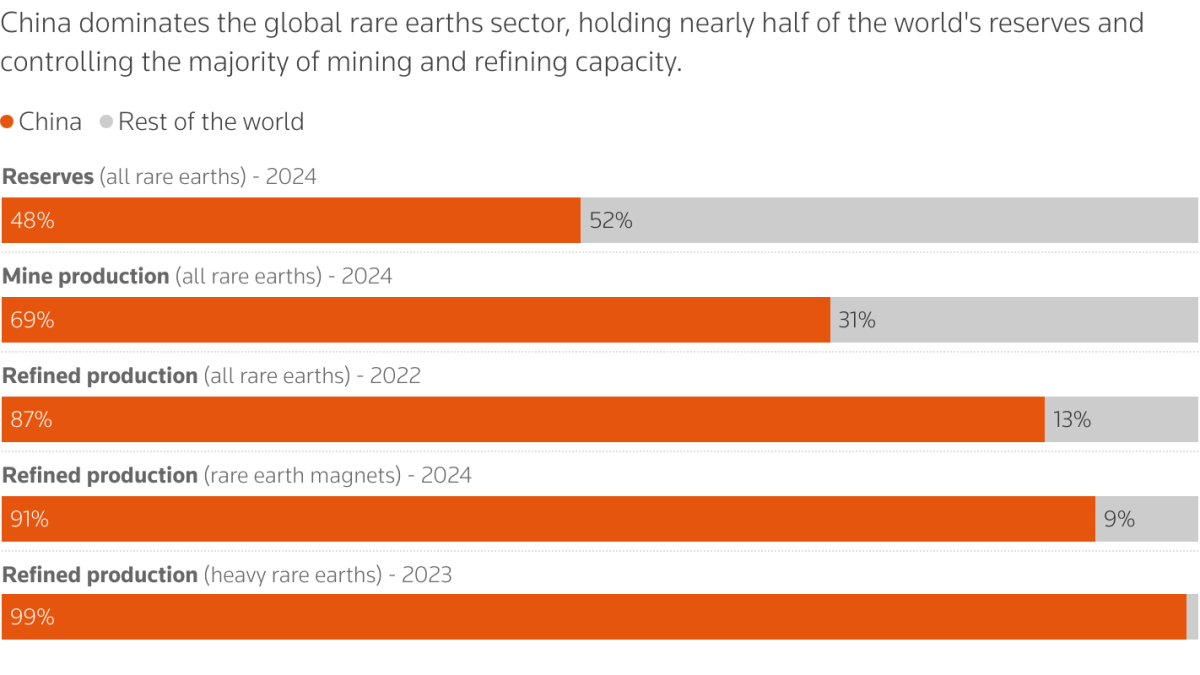

When shoppers purchase electric vehicles or smartphones, few consider the journey of metals hidden inside these devices. While headlines often focus on China’s grip on rare earth elements, another industrial dominance has been quietly growing stronger without much fanfare.

The copper flowing through the wires of modern technology increasingly passes through Chinese refineries before reaching global markets. This shift represents more than just industrial capacity – it signals a fundamental change in how one of civilization’s most essential metals moves around the world.

What started as an extension of China’s manufacturing boom has evolved into something far more strategic, creating new dependencies that ripple through supply chains from construction sites in California to renewable energy projects in Germany.

China’s Copper Refining Capacity Surpasses Global Competitors

China now processes nearly half of the world’s refined copper, a dramatic increase from just 15% two decades ago. The country’s refining capacity has grown from 2.8 million tons in 2005 to over 12 million tons today, dwarfing traditional copper powerhouses like Chile and Peru.

This expansion wasn’t accidental. Chinese companies systematically invested in refining infrastructure while Western nations focused on mining operations. The strategy proved prescient as global demand for refined copper soared alongside the digital revolution and green energy transition.

Major Chinese refineries like Jiangxi Copper Company and Tongling Nonferrous Metals have become household names in commodity circles. These facilities don’t just process domestic ore – they import raw materials from mines worldwide, adding value before re-exporting finished copper products.

The scale advantage allows Chinese refineries to operate with lower per-unit costs than smaller facilities elsewhere. This economic efficiency creates a gravitational pull, drawing more raw copper concentrate toward Chinese processing centers year after year.

| Country | Copper Refining Capacity (Million Tons) | Global Market Share | Change Since 2010 |

|---|---|---|---|

| China | 12.2 | 47% | +85% |

| Chile | 2.1 | 8% | +15% |

| Japan | 1.8 | 7% | -5% |

| United States | 1.2 | 5% | -20% |

| Germany | 0.9 | 3% | -10% |

Strategic Acquisitions Extend Chinese Influence Across Supply Chains

Chinese companies haven’t limited themselves to domestic refining capacity. Strategic acquisitions of mining operations and processing facilities worldwide have created an integrated supply network spanning continents. State-owned enterprises and private companies alike have purchased stakes in copper mines from Africa to South America.

Zijin Mining Group’s acquisition of Serbia’s Bor copper mine exemplifies this approach. The $1.26 billion investment not only secured copper concentrate supplies but also brought European refining capabilities under Chinese control. Similar deals have unfolded across multiple continents, often targeting distressed assets that Western companies couldn’t profitably operate.

These acquisitions create vertical integration opportunities unavailable to competitors. Chinese refineries can now coordinate directly with captive mines, optimizing logistics and ensuring steady raw material flows. This integration provides cost advantages and supply security that independent refineries struggle to match.

The ownership structure also enables long-term strategic planning that publicly traded Western companies find difficult to justify to shareholders. Chinese firms can accept lower short-term returns while building market position, a luxury that transforms competitive dynamics across the industry.

*In global commodities, control over processing often matters more than owning the raw materials.*

Technology Transfer Accelerates Refining Efficiency Gains

Chinese copper refineries have rapidly adopted and improved upon international best practices, often surpassing original technology providers in operational efficiency. Joint ventures with European and Japanese companies initially brought advanced smelting techniques to China, but technology transfer soon flowed in both directions.

Modern Chinese facilities now operate some of the world’s most efficient copper smelting operations. Automated systems, advanced environmental controls, and continuous process improvements have reduced energy consumption while increasing output quality. These technological gains provide sustainable competitive advantages beyond simple labor cost differences.

Innovation extends to recycling capabilities as well. Chinese refineries have become increasingly sophisticated at processing electronic waste and scrap copper, creating additional feed sources that reduce dependence on mined ore. This circular economy approach aligns with government sustainability goals while providing cost-effective raw materials.

Environmental compliance has also improved dramatically as Chinese facilities adopt cleaner production methods. While legacy pollution issues persist at older sites, new refineries often exceed international environmental standards, dispelling outdated assumptions about Chinese industrial practices.

“Chinese copper refineries have invested heavily in clean technology and automation over the past decade. Their newest facilities rival anything we see in developed markets,” notes Dr. Sarah Chen, metals industry analyst at Global Commodity Research Institute.

Global Supply Chains Increasingly Depend on Chinese Processing

The concentration of copper refining in China has created dependencies that extend far beyond the metal itself. Manufacturers worldwide now rely on Chinese-processed copper for everything from electrical wiring to renewable energy infrastructure. This dependency becomes particularly acute during supply disruptions or geopolitical tensions.

European automakers, despite efforts to diversify supply chains, still source significant amounts of refined copper from Chinese facilities. The metal’s journey often involves ore mined in South America, shipped to China for processing, then exported as finished copper products to European manufacturing plants. This circuitous route reflects economic realities more than political preferences.

Construction industries globally have similarly adapted to Chinese copper supply patterns. Major infrastructure projects often specify copper products that trace back to Chinese refineries, not because of deliberate sourcing decisions but due to market availability and competitive pricing. Alternative suppliers frequently cannot match Chinese capacity or delivery schedules.

The renewable energy sector faces particular challenges given copper’s central role in wind turbines, solar panels, and electric vehicle batteries. Green energy projects promoting energy independence often rely on copper processed in China, creating an ironic dependency that complicates sustainability narratives.

| Industry Sector | Copper Dependency on China | Alternative Sources | Supply Risk Level |

|---|---|---|---|

| Electric Vehicles | 65% | Limited | High |

| Construction | 45% | Moderate | Medium |

| Electronics | 55% | Limited | High |

| Power Grid | 40% | Moderate | Medium |

| Renewable Energy | 60% | Limited | High |

*Supply chains, like rivers, naturally flow toward the most efficient processing centers.*

Geopolitical Tensions Highlight Strategic Vulnerabilities

Recent trade disputes and geopolitical tensions have exposed the strategic implications of concentrated copper refining capacity. While China has not weaponized copper supplies like it has rare earths, the theoretical potential creates anxiety among policymakers in import-dependent nations.

The COVID-19 pandemic provided a preview of potential disruption scenarios when Chinese refinery operations temporarily reduced due to lockdowns. Copper prices spiked globally as markets recognized the concentration risk, leading to renewed discussions about supply chain diversification among government and industry leaders.

Military strategists have begun incorporating copper supply scenarios into national security assessments. Modern weapons systems, communication networks, and defense infrastructure all require substantial copper inputs, making refining capacity a consideration in strategic planning processes.

Trade negotiators increasingly view industrial metals as strategic assets rather than simple commodities. Discussions about critical mineral security now routinely include copper alongside rare earths and lithium, reflecting growing awareness of processing bottlenecks and geographic concentration risks.

“We’ve seen how quickly supply chain disruptions can cascade through the global economy. Copper refining represents a significant chokepoint that deserves the same policy attention as semiconductor manufacturing,” explains former U.S. Trade Representative advisor Michael Torres.

Environmental Standards Create Barriers for Alternative Refineries

Establishing new copper refineries outside China faces significant environmental and regulatory hurdles that favor existing operations. Modern environmental standards require extensive pollution control systems that add substantial capital costs to new projects. Chinese facilities, having already made these investments, enjoy incumbency advantages.

Permitting processes for new smelters can take years in developed countries, during which time Chinese capacity continues expanding to meet growing demand. Community opposition to industrial facilities creates additional delays and costs that make alternative refinery projects financially challenging for private investors.

Legacy environmental liabilities at former copper processing sites in North America and Europe create cautionary tales that discourage new investments. Cleanup costs from older facilities can exceed original construction expenses, making investors wary of long-term environmental risks associated with copper refining operations.

China’s willingness to accept environmental trade-offs during its industrialization phase allowed rapid capacity development that would be impossible under current Western environmental standards. While Chinese environmental enforcement has strengthened significantly, existing facilities benefit from grandfather clauses and established infrastructure investments.

*Environmental protection and industrial policy often create unintended strategic consequences.*

Market Dynamics Reinforce Chinese Dominance

Economic forces continue strengthening China’s position in copper refining despite concerns about over-concentration. Chinese domestic demand for refined copper consumes roughly 60% of global production, providing local refineries with captive markets that ensure capacity utilization even during export disruptions.

Scale economies in copper refining create self-reinforcing advantages for large operations. Fixed costs for environmental systems, energy infrastructure, and skilled personnel spread across larger volumes result in lower per-unit costs that smaller refineries cannot match. This dynamic naturally concentrates production in the largest facilities.

Financial markets have adapted to Chinese dominance by pricing copper futures based on Chinese demand patterns and refinery operations. The Shanghai Futures Exchange now rivals the London Metal Exchange in copper price discovery, reflecting China’s central role in physical markets.

International mining companies increasingly orient their operations toward Chinese refinery customers, adapting ore specifications and delivery schedules to Chinese requirements. This customer focus reinforces Chinese bargaining power and makes it more difficult for alternative refineries to secure competitive raw material supplies.

“Market forces strongly favor concentration in copper refining. Unless governments actively intervene with subsidies or trade policies, Chinese dominance will likely continue growing,” observes commodity markets specialist Dr. James Richardson from the International Mining Economics Institute.

Industry Responses and Diversification Efforts

Some companies and governments have launched initiatives to reduce dependence on Chinese copper refining, though progress remains limited compared to the scale of the challenge. The European Union’s Critical Raw Materials Act includes provisions for developing regional copper processing capabilities, while the United States has provided tax incentives for domestic metal refining investments.

Private sector responses have focused primarily on long-term supply contracts and strategic partnerships rather than new facility construction. Some large consumers have negotiated direct relationships with non-Chinese refineries to secure alternative supply sources, though at premium prices that reflect limited capacity outside China.

Recycling initiatives have gained traction as a way to reduce dependence on primary copper refining. Advanced recycling technologies can process electronic waste and industrial scrap into high-purity copper without traditional smelting processes, potentially creating more distributed processing capabilities.

Joint venture approaches have emerged between Western companies and Chinese partners to develop refining capacity in third countries. These partnerships attempt to combine Chinese technical expertise and capital with Western market access and raw material supplies, though political sensitivities complicate such arrangements.

Future Implications for Global Copper Markets

Current trends suggest Chinese dominance in copper refining will likely strengthen over the next decade unless significant policy interventions alter market dynamics. Chinese domestic demand growth, continued investment in refining capacity, and advantages from existing scale create powerful momentum favoring further concentration.

Climate change policies may paradoxically increase dependence on Chinese copper refining despite diversification intentions. The massive copper requirements for renewable energy infrastructure and electric vehicle adoption exceed current non-Chinese refining capacity, potentially forcing even reluctant consumers to rely on Chinese supplies.

Technological developments in copper recycling and alternative processing methods could eventually provide pathways to reduced Chinese dependence, but such changes require years of development and substantial capital investment. Current recycling technologies handle only a fraction of global copper demand, leaving primary refining as the dominant supply source.

Geopolitical tensions may accelerate efforts to develop alternative refining capacity through government support and strategic partnerships. However, the economic fundamentals that created Chinese dominance remain unchanged, suggesting that alternative capacity will require ongoing subsidies or trade protection to remain competitive.

*Strategic dependencies, once established, prove remarkably difficult to unwind without sustained political commitment.*

Why has China become dominant in copper refining?

China’s dominance stems from massive investments in refining capacity, domestic demand growth, strategic acquisitions of global mining assets, and scale economies that reduce per-unit processing costs compared to smaller international competitors.

How much of global copper refining does China control?

China currently processes approximately 47% of the world’s refined copper, up from just 15% two decades ago. This represents over 12 million tons of annual refining capacity.

What industries are most affected by Chinese copper refining dominance?

Electric vehicles, electronics, renewable energy, and construction industries face the highest dependency levels on Chinese-processed copper, with some sectors sourcing over 60% of their copper from Chinese refineries.

Are there alternatives to Chinese copper refining?

Limited alternatives exist in Chile, Japan, the United States, and Germany, but combined capacity falls short of Chinese levels. Building new refineries faces environmental, regulatory, and economic challenges.

Could China restrict copper exports like it has with rare earths?

While China hasn’t restricted copper exports, the theoretical potential exists. However, China’s large domestic consumption means export restrictions would also impact Chinese manufacturers and economic growth.

What are governments doing to reduce copper refining dependence?

The EU and United States have launched critical materials initiatives including tax incentives for domestic refining, strategic partnerships, and recycling programs, though progress remains limited compared to Chinese capacity.

How do environmental regulations affect copper refining location?

Strict environmental standards in developed countries increase costs and delays for new refineries, while existing Chinese facilities benefit from prior investments and established infrastructure.

What role does recycling play in copper supply security?

Recycling provides some supply diversification but currently handles only a fraction of global demand. Advanced recycling technologies could eventually reduce dependence on primary refining.

How does Chinese copper dominance compare to rare earth control?

While China controls roughly 80% of rare earth processing versus 47% of copper refining, copper’s much larger market size and broader industrial applications make the dependency more economically significant.

Will renewable energy increase dependence on Chinese copper?

Yes, renewable energy infrastructure requires massive copper inputs that likely exceed current non-Chinese refining capacity, potentially forcing greater reliance on Chinese processors despite diversification goals.

What are the main barriers to building new copper refineries?

Major barriers include high capital costs, lengthy permitting processes, environmental compliance requirements, community opposition, and difficulty competing with Chinese scale economies.

How do financial markets reflect Chinese copper dominance?

Copper prices increasingly reflect Chinese demand patterns and refinery operations, with Shanghai futures markets rivaling London in price discovery, demonstrating China’s central role in global copper markets.