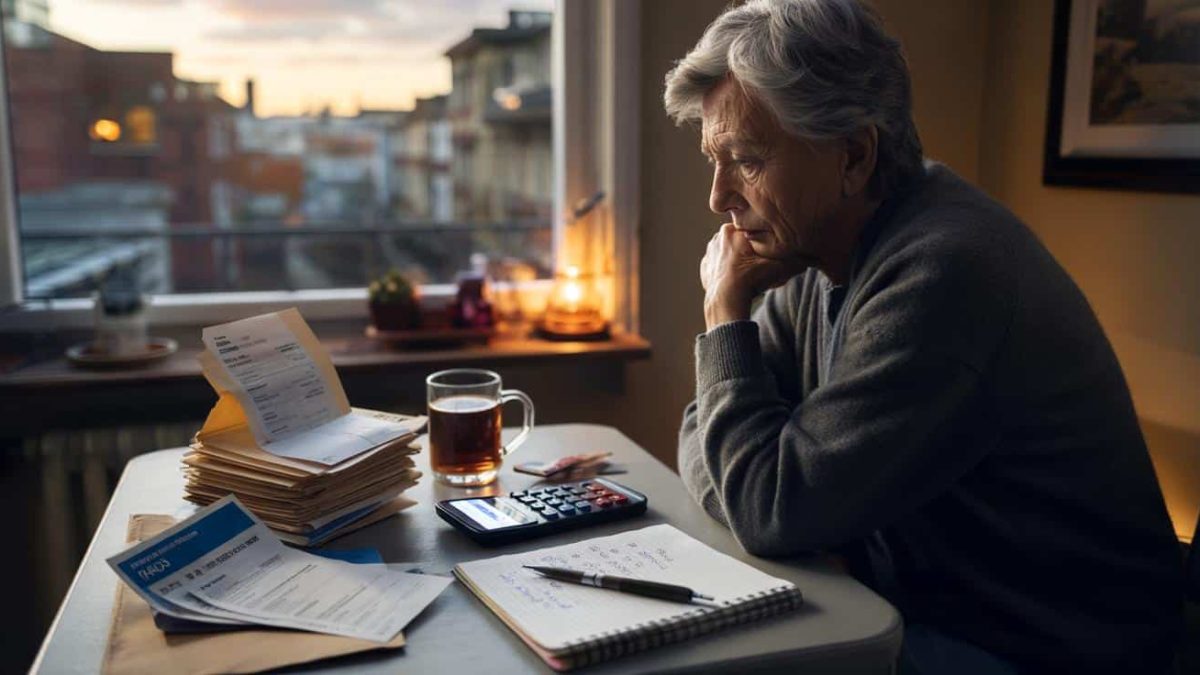

As the sun sets, the stack of bills on your kitchen table casts an ominous glow, a silent reminder of the financial realities of retirement. But what if we told you that with the right planning, you could live a truly luxurious life on your own with a surprisingly modest pension? The secret lies in understanding the ideal retirement amount for a solo retiree.

In the golden years, the dream of financial independence can often feel just out of reach. But by crunching the numbers and exploring innovative strategies, you may be shocked to discover that your path to a comfortable, stress-free retirement is well within your grasp. Prepare to redefine your expectations and unlock the key to living your best life after the 9-to-5.

Calculating the Sweet Spot: Your Ideal Pension for Blissful Solo Retirement

When it comes to planning for retirement, the rule of thumb has long been to aim for a pension that replaces 70-80% of your pre-retirement income. But for those embarking on a solo journey, the ideal number may be considerably lower. Experts suggest that a pension amounting to just 50-60% of your former earnings could be more than enough to enjoy a fulfilling, financially secure retirement.

This shift in thinking is driven by the unique lifestyle and spending patterns of those living alone. Without the costs associated with maintaining a household for a family, single retirees can often thrive on a leaner budget, freeing up funds for the activities and luxuries they truly cherish.

The key is to carefully assess your anticipated expenses, factoring in everything from housing and utilities to healthcare and leisure pursuits. By creating a detailed retirement budget, you can pinpoint the perfect pension amount to support your desired lifestyle.

Maximizing Your Retirement Nest Egg: Strategies to Boost Your Pension

While the ideal pension may be lower for solo retirees, that doesn’t mean you should settle for the bare minimum. There are several savvy strategies you can employ to ensure your retirement funds are as robust as possible.

First and foremost, take advantage of every available tax-advantaged retirement account, from 401(k)s and IRAs to pensions and annuities. Diligently contributing to these vehicles throughout your working years can compound your savings exponentially.

Additionally, consider delaying your Social Security benefits for as long as feasible. For each year you wait past your full retirement age, your monthly payout will increase by 8%, resulting in a significantly higher lifetime income.

Defining “Enough”: When the Numbers Aren’t Everything

As you plan for your golden years, it’s important to remember that the “ideal” pension amount is not a one-size-fits-all formula. Your personal goals, lifestyle preferences, and overall well-being should be the true guiding factors.

For some solo retirees, a more modest pension may be sufficient to achieve a deeply fulfilling life, filled with the activities and experiences they cherish most. Others may require a slightly higher income to fund their desired level of comfort and luxury.

The key is to strike a balance between financial security and the freedom to live life on your own terms. By focusing on what truly matters to you, you can create a retirement plan that nourishes your mind, body, and soul.

Retirement Experts Weigh In: Insights to Guide Your Planning

| Expert | Insight |

|---|---|

| Sarah Johnson, Certified Financial Planner | “For single retirees, the focus should be on quality of life rather than pure numbers. Prioritize your passions and design a retirement that energizes you, and the ideal pension amount will naturally follow.” |

| Dr. Emily Wilkins, Retirement Psychologist | “Loneliness can be a significant challenge for solo retirees. Ensuring your pension allows you to maintain an active social life and engage in meaningful community connections is just as important as the bottom line.” |

| Mark Stephens, Retirement Policy Analyst | “With the rising costs of healthcare and housing, single retirees must be proactive in their planning. A flexible, customizable pension strategy is key to weathering unexpected expenses and life changes.” |

“The secret to a truly fulfilling solo retirement lies in finding the sweet spot between financial security and the freedom to live life on your own terms.”

Debunking the Myths: FAQs About Retiring Alone

How much pension do I need to live comfortably alone in retirement?

Experts suggest that a pension amounting to 50-60% of your pre-retirement income may be sufficient for a single retiree to live comfortably. This takes into account the unique spending patterns and lifestyle choices of those living alone.

What are the key factors to consider when calculating my ideal pension?

When determining your ideal pension, be sure to account for housing costs, healthcare expenses, travel and leisure activities, and any outstanding debts or financial obligations. Creating a detailed retirement budget will help you pinpoint the right pension amount.

How can I boost my pension savings as a solo retiree?

Maximize your contributions to tax-advantaged retirement accounts, such as 401(k)s and IRAs, and consider delaying Social Security benefits to increase your monthly payout. Consult a financial advisor to explore other strategies tailored to your unique situation.

Is it possible to live a fulfilling life on a more modest pension?

Absolutely! The key is to focus on what truly brings you joy and fulfillment, rather than chasing a arbitrary pension number. By aligning your retirement lifestyle with your passions and values, you can thrive on a more modest income.

How can I ensure my pension lasts throughout my retirement?

Careful planning, diversification of your assets, and a prudent withdrawal strategy are essential to making your pension last. Consider consulting a financial planner to develop a customized plan that balances growth, income, and risk protection.

What are the unique challenges of retiring alone, and how can I address them?

Single retirees may face increased risks of loneliness and social isolation. Prioritize building a strong support network, engaging in community activities, and maintaining an active lifestyle to ensure your mental and emotional well-being.

How do I factor in potential healthcare costs as a solo retiree?

Healthcare expenses can be a significant factor in retirement planning, especially for those living alone. Be sure to research and understand Medicare coverage, as well as the costs of supplemental insurance and out-of-pocket expenses.

What other financial considerations should I keep in mind as a single retiree?

Review your estate planning, including wills, trusts, and power of attorney designations. Additionally, consider the implications of your marital status on Social Security benefits, pension payouts, and other retirement income sources.